What are Fringe Benefits?

Fringe benefits are a way to compensate your employees beyond their regular wages. These perks, like gym memberships and cell phone reimbursements, can help your business attract and retain talented employees by adding to their overall compensation.What is imputed income?

For tax purposes, imputed income is the fair market value of non-cash compensation that business owners give to employees, which can be in the form of perks known as fringe benefits.

This income is added to an employee’s gross wages so employment taxes can be withheld. Imputed income is not included in an employee’s net pay since the benefit was already given separately in a non-monetary form.

For more information about employees and imputed earning, see the IRS Employer’s Tax Guide to Fringe Benefits.

Examples of imputed income

Most imputed income must be taxed. Examples of imputed earnings include:

- Memberships for gyms, wellness programs, health clubs and country clubs

- Personal use of a company or employer-provided vehicle

- Gift cards, awards and prizes, regardless of the dollar amount

- Group-term life insurance valued at more than $50,000

- Educational financial assistance and tuition reimbursement exceeding $5,250

- Dependent care assistance exceeding $5,000

- Adoption assistance exceeding the tax-free amount

- Moving expense reimbursements that are nondeductible

Examples of nontaxable fringe benefits

Benefits below a certain value may be considered nontaxable by the IRS, because these benefits have so little monetary value that accounting for them would be administratively impracticable. Typically these benefits have a value of less than $100. Benefits valued at $100 or more are not exempt and must be reported.

Examples of nontaxable fringe benefits can include:

- Occasional tickets for sporting events and theaters

- Picnics and parties for employees and their guests

- Birthday and holiday gifts with a low market value (except for cash)

- Occasional personal use of an employer-provided cell phone

- Meals and meal money provided when employees work overtime

- Occasional local transportation fares for employees working overtime

- Public transportation passes that don’t exceed a discount of $21 per month

- Company logo-branded items of low value, such as pens, shirts, keychains and water bottles

- Occasional personal use of the company copying machine

- Health savings accounts

- Group-term life insurance for the employee’s spouse or dependent, not exceeding a face amount of $2,000

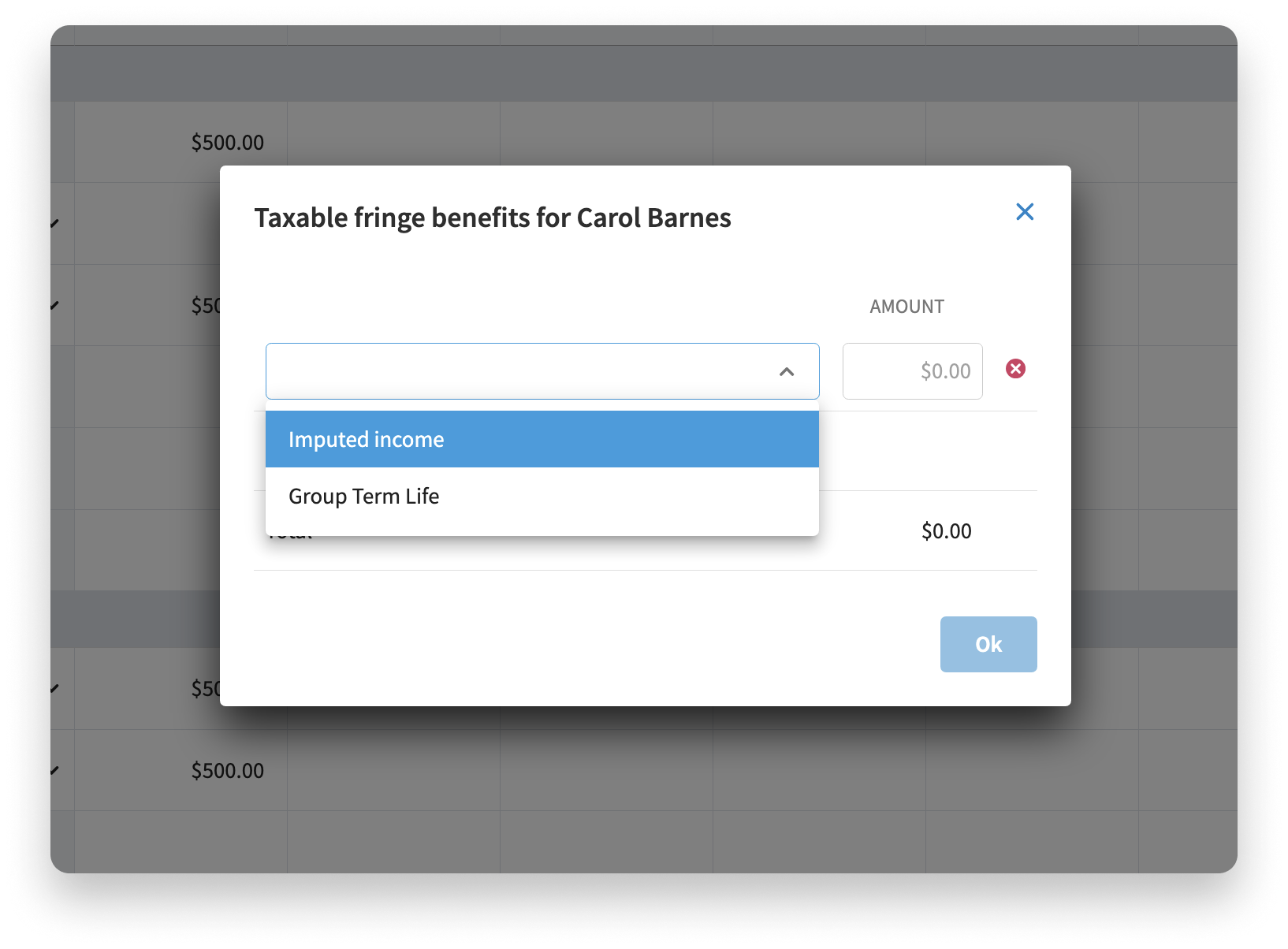

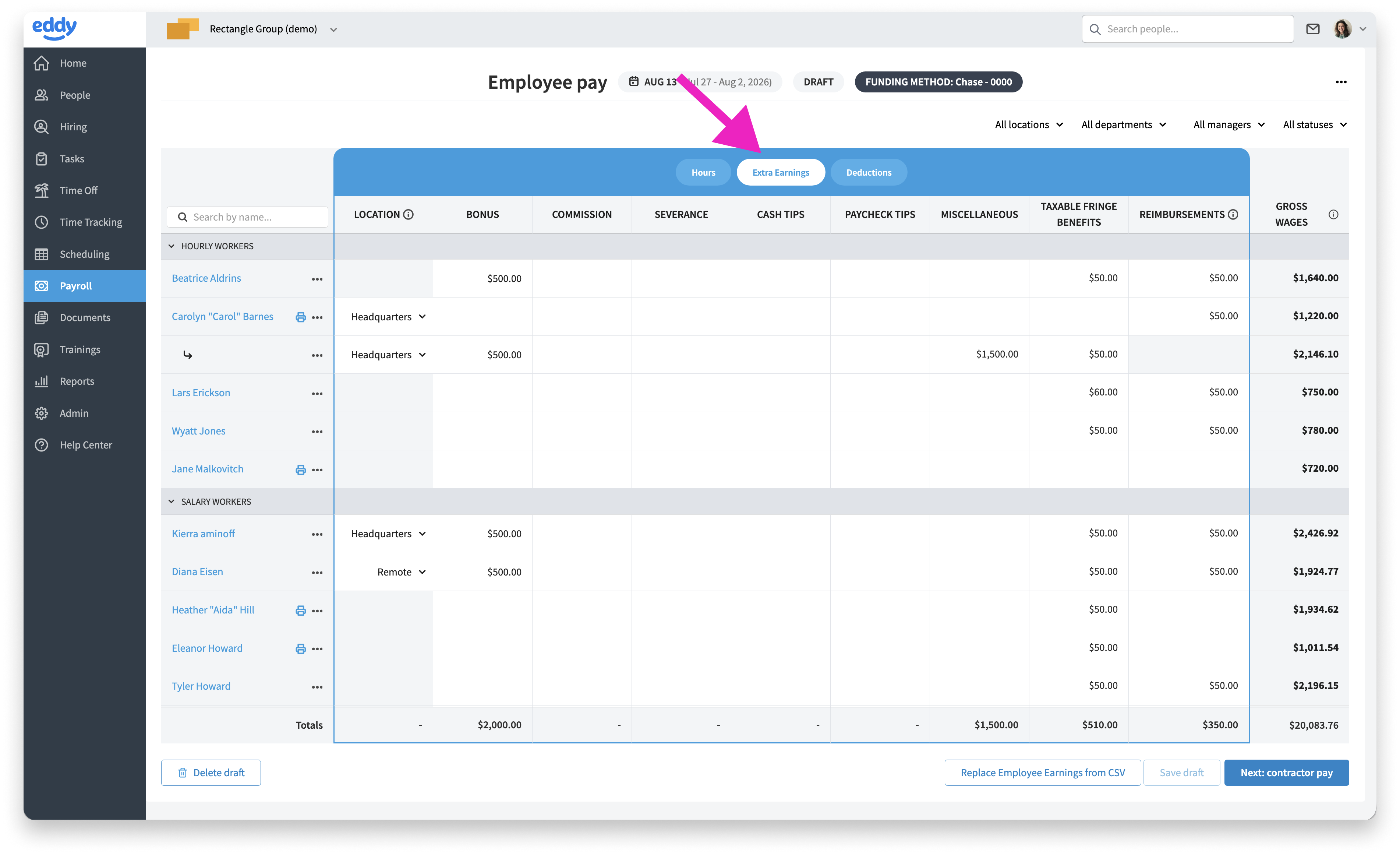

How to enter imputed income in Eddy payroll

To enter imputed income in Eddy payroll go to the Extra earnings page.

Look for the column labeled Taxable Fringe Benefits. As you hover your mouse in that column you'll see a pencil icon to edit the info for the worker. Click the pencil icon to view the taxable fringe benefits dialog box. You can choose to enter either Imputed income or Group Term life.